The Nikkei 225’s record-breaking surge following Sanae Takaichi’s election victory signals more than a localized political shift; it represents a fundamental repricing of Japanese risk and a departure from the "normalization" path previously projected by the Bank of Japan (BoJ). Investors are not merely reacting to a change in leadership, but to the decisive removal of the "Ishiba Shock" risk—the fear of hiked corporate taxes and aggressive interest rate hikes. This rally is underpinned by a transition from a monetary policy focused on stabilization to a fiscal-monetary coordination aimed at ending three decades of deflationary psychology through aggressive expansion.

The Triad of Pro-Growth Volatility

The market’s violent upward correction functions through three distinct transmission mechanisms: currency-driven export competitiveness, the preservation of the negative real interest rate environment, and the anticipated expansion of the "New Capitalism" framework toward pure supply-side incentives.

1. The Yen-Nikkei Inverse Correlation

Takaichi’s vocal opposition to premature interest rate hikes serves as a ceiling for the Yen. In a global macro environment where the US Federal Reserve has begun its easing cycle, a hawkish BoJ would have triggered a rapid narrowing of the interest rate differential, causing the Yen to appreciate and crushing the earnings of Japan’s heavy exporters. By signaling a commitment to the "Takaichi-nomics" doctrine—a more aggressive evolution of Abenomics—the administration has effectively re-established the Yen as a carry-trade favorite, providing a floor for the Nikkei’s multinational components.

2. The Real Rate Compression

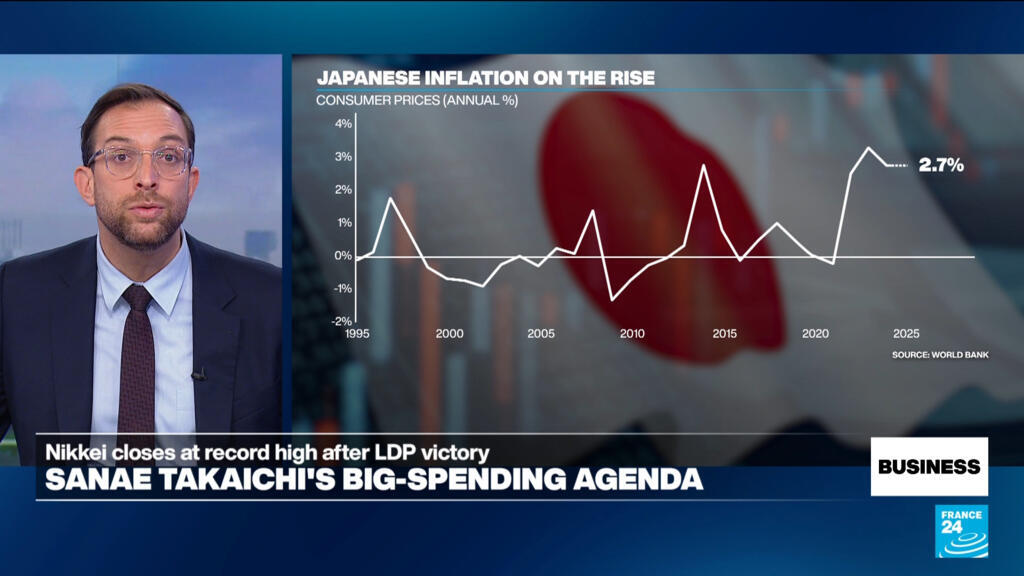

Inflation in Japan is currently hovering near or above the 2% target, yet nominal yields remain suppressed.

Takaichi’s victory ensures that nominal rates will likely lag behind inflation for a longer duration than previously forecasted. This creates deeply negative real interest rates, which fundamentally alters the discounted cash flow (DCF) models for Japanese equities. When the real cost of capital is negative, equity risk premiums become exceptionally attractive, forcing a rotation from Japanese Government Bonds (JGBs) and cash into the equity market.

3. Supply-Side Fiscal Multipliers

Unlike her predecessors who balanced growth with "fiscal health" (a euphemism for consumption tax hikes), Takaichi’s platform prioritizes strategic investment in high-tech sectors—specifically semiconductors, fusion energy, and quantum computing. This shifts the government’s role from a passive regulator to an active venture partner, reducing the "hurdle rate" for private sector R&D and attracting foreign direct investment (FDI) that had been sidelined by political uncertainty.

Analyzing the Sectoral Winners and Losers

The capital inflow following the election result is not uniform. A granular analysis reveals a divergence between "Old Japan" value stocks and "New Japan" growth entities, dictated by their sensitivity to debt-servicing costs and global trade flows.

- Export-Oriented Manufacturing: Automotive and precision machinery sectors are the primary beneficiaries of the Yen’s weakness. These firms carry high operating leverage; a 1-yen move against the dollar can result in billions of yen in additional operating profit.

- Technology and Defense: Takaichi’s emphasis on "Economic Security" acts as a direct subsidy for domestic defense contractors and cybersecurity firms. We are seeing a structural shift where these companies are no longer viewed as static utilities but as high-growth strategic assets.

- Banking and Financials: This sector represents a point of friction. While a rising Nikkei generally boosts sentiment, the delay in interest rate normalization harms the net interest margins (NIM) of major lenders. The rally in bank stocks is therefore a bet on increased loan volume driven by a booming economy, rather than higher spreads on existing capital.

The Risk of Debt Sustainability and Policy Overstretch

The primary constraint on this bullish thesis is the Japanese fiscal position. With a debt-to-GDP ratio exceeding 250%, the Takaichi administration is operating within a narrow corridor.

The first limitation of this strategy is the "Bond Vigilante" risk. If the market perceives that the BoJ has lost its independence to the Prime Minister’s Office, JGB yields could spike despite official policy, leading to a destabilizing decoupling of the bond and equity markets. This would force the BoJ into an unsustainable program of Yield Curve Control (YCC) 2.0, effectively monetizing the deficit at the cost of extreme currency debasement.

The second bottleneck is "Imported Inflation." A weak Yen is a double-edged sword. While it aids exporters, it raises the cost of energy and food imports, which are denominated in dollars. This puts a squeeze on the Japanese consumer. If real wages do not keep pace with this cost-push inflation, the Nikkei’s gains may be hollow, reflecting currency devaluation rather than genuine value creation. The durability of the record highs depends entirely on whether corporate Japan can translate increased profits into a sustained wage-price spiral.

Operational Strategy for Institutional Allocators

For the global investor, the record-breaking Nikkei is not a signal to "buy the index" indiscriminately. The play is a targeted exposure to the "Strategic Autonomy" theme.

First, prioritize companies with high "Pricing Power." As inflation becomes a permanent feature of the Japanese economy for the first time in a generation, firms that can pass costs to consumers without losing volume will outperform. Retailers with premium branding and tech firms with proprietary intellectual property are the ideal vehicles.

Second, monitor the 10-year JGB yield as a proxy for the "Takaichi Premium." A steady yield alongside a rising Nikkei indicates the market trusts the administration’s ability to manage the transition. A volatile yield indicates the "Abenomics 2.0" experiment is overheating.

Third, hedge the Yen exposure. The Nikkei’s record is partially a "nominal" record driven by currency weakness. To capture "alpha" in dollar terms, investors must utilize currency-hedged ETFs or direct FX forwards to strip out the depreciation of the Yen from the equity gains.

The record high of the Nikkei is the market’s way of pricing in a high-conviction bet on the end of Japanese stagnation. However, the move from a deflationary equilibrium to an inflationary growth model is inherently volatile. The strategic move is to position in the sectors that act as the backbone of Takaichi’s economic security agenda—semiconductors and defense—while maintaining a liquid hedge against the inevitable test of the BoJ’s resolve by global bond markets. Focus on the spread between nominal growth and nominal yields; as long as growth leads, the Nikkei has significant room to run beyond this record.