You've likely heard the chatter about the "end of dollar dominance." It's a favorite headline for analysts watching China’s economic climb. With the expansion of the Cross-Border Interbank Payment System (CIPS) and more trade being settled in Renminbi (RMB), the narrative suggests the US dollar is on its last legs. But if you look at the actual plumbing of global finance, that story falls apart. China is building a formidable alternative for its allies, but a "backup system" isn't the same thing as a new world standard.

The reality is that Beijing is caught in a trap of its own making. They want the prestige and power of a global currency without the one thing that makes a currency global: giving up control. As long as the Chinese Communist Party (CCP) prioritizes stability and capital controls over a free-floating exchange rate, the RMB will remain a niche player on the world stage.

The CIPS Illusion

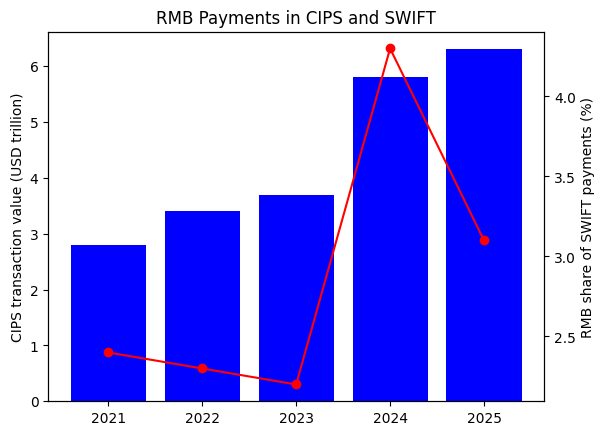

CIPS is often framed as China’s answer to SWIFT. That’s not quite right. SWIFT is a messaging system; it doesn't move the money, it just sends the instructions. CIPS, on the other hand, is a clearing and settlement system. In 2026, CIPS has grown to nearly 200 direct participants, a 40% jump from just two years ago. On the surface, this looks like a massive shift away from Western infrastructure.

Don't be fooled by the participant list. About 80% of CIPS transactions still rely on SWIFT’s messaging layer to function. It’s more of an "add-on" than a replacement. Even with the growth, CIPS processed roughly $24 trillion in 2024. That sounds huge until you realize SWIFT handles quadrillions. The scale isn't even in the same ballpark.

China’s push for CIPS is largely about "sanction-proofing." After seeing Russia get frozen out of the dollar system, Beijing realized they needed a fire escape. If you're a country like Iran or Russia, CIPS is a lifeline. If you're a global bank in London or New York, it’s just another pipe you might use occasionally to keep your Chinese clients happy.

The Problem With Closed Doors

If you want to be the world’s reserve currency, people have to be able to get their money out as easily as they put it in. China doesn't allow that. The "Capital Account" remains tightly guarded.

I’ve talked to plenty of treasury managers who are hesitant to hold large amounts of RMB. Why? Because the People’s Bank of China (PBOC) can change the rules overnight. In 2025, we saw a continued trend of "managed" depreciation to keep exports competitive. If you’re a central bank in Brazil or Indonesia, you don't want your reserves to lose value just because Beijing needs to hit a GDP target.

- USD Share of Global Payments: Still hovering around 47%.

- RMB Share of Global Payments: Recently hit 4.7%, but usually fluctuates between 2.8% and 5%.

- USD in Global Reserves: Roughly 58-59%.

- RMB in Global Reserves: Barely 2.3%.

The gap is a chasm. The dollar isn't dominant because of some conspiracy; it’s dominant because it’s liquid. You can buy anything from oil to iPhones to Iowa corn with dollars. You can’t do that with RMB yet.

Trade Settlement vs Reserve Power

China has been successful in one specific area: trade settlement. More than half of China’s own cross-border trade is now done in its own currency. That’s a smart move for them. It reduces their dependence on the dollar for their own imports and exports.

However, using a currency to buy a shipment of soybeans isn't the same as using it to store your nation's wealth. To be a reserve currency, you need deep, transparent bond markets. The US Treasury market is the deepest in the world. Even with US political drama, it remains the "risk-free" asset of choice. China’s bond market is growing, but it lacks the transparency and legal protections that global investors demand.

[Image comparing the liquidity of US Treasury vs Chinese Government Bond markets]

The CCP faces a "Trilemma." They want a stable exchange rate, independent monetary policy, and free capital flow. You can only have two. China chose the first two and sacrificed the third. Until they let the RMB float freely, it’s going to stay in the junior varsity league.

The Geopolitical Firewall

Western sanctions have actually done China a favor by forcing "renegade states" into the RMB ecosystem. Russia, Iran, and parts of the Middle East are now the primary testing grounds for the "Digital Yuan" (e-CNY) and CIPS.

This is creating a "dual-rail" financial world. One rail is the dollar-based system used by the G7 and most of the developing world. The other is a China-centric rail for those who either don't like the US or have been kicked out of its club. This doesn't destroy the dollar; it just limits its reach in specific corners of the globe.

Honestly, the biggest threat to the dollar isn't the RMB. It's the US itself. Irresponsible fiscal policy and the over-use of financial sanctions are the only things that could truly drive the world away from the greenback. But even then, there isn't a better alternative waiting in the wings. The Euro has its own structural flaws, and the RMB comes with too many strings attached.

How to Position Your Business

If you're managing a company with significant exposure to Chinese markets, you shouldn't ignore CIPS, but don't bet the farm on it either.

- Dual-Pathing: Ensure your banking partners have CIPS connectivity for your China-based operations to avoid delays.

- Hedge Currency Risks: Don't treat RMB like a stable asset. It's a policy tool for the PBOC. Use hedging instruments to protect against sudden devaluations.

- Watch the BRICS+ Expansion: As more countries join this bloc, expect more bilateral trade deals in local currencies. This won't replace the dollar, but it will change how you invoice certain regions.

The dollar's "death" is a myth that gets clicks but lacks substance. China is building a powerful regional system, but as long as they prioritize control over openness, the dollar's crown is safe.

Review your current currency exposure for 2026. If you're over-reliant on any single "fire escape" system like CIPS, diversify your banking rails to ensure liquidity isn't tied to a single political regime.