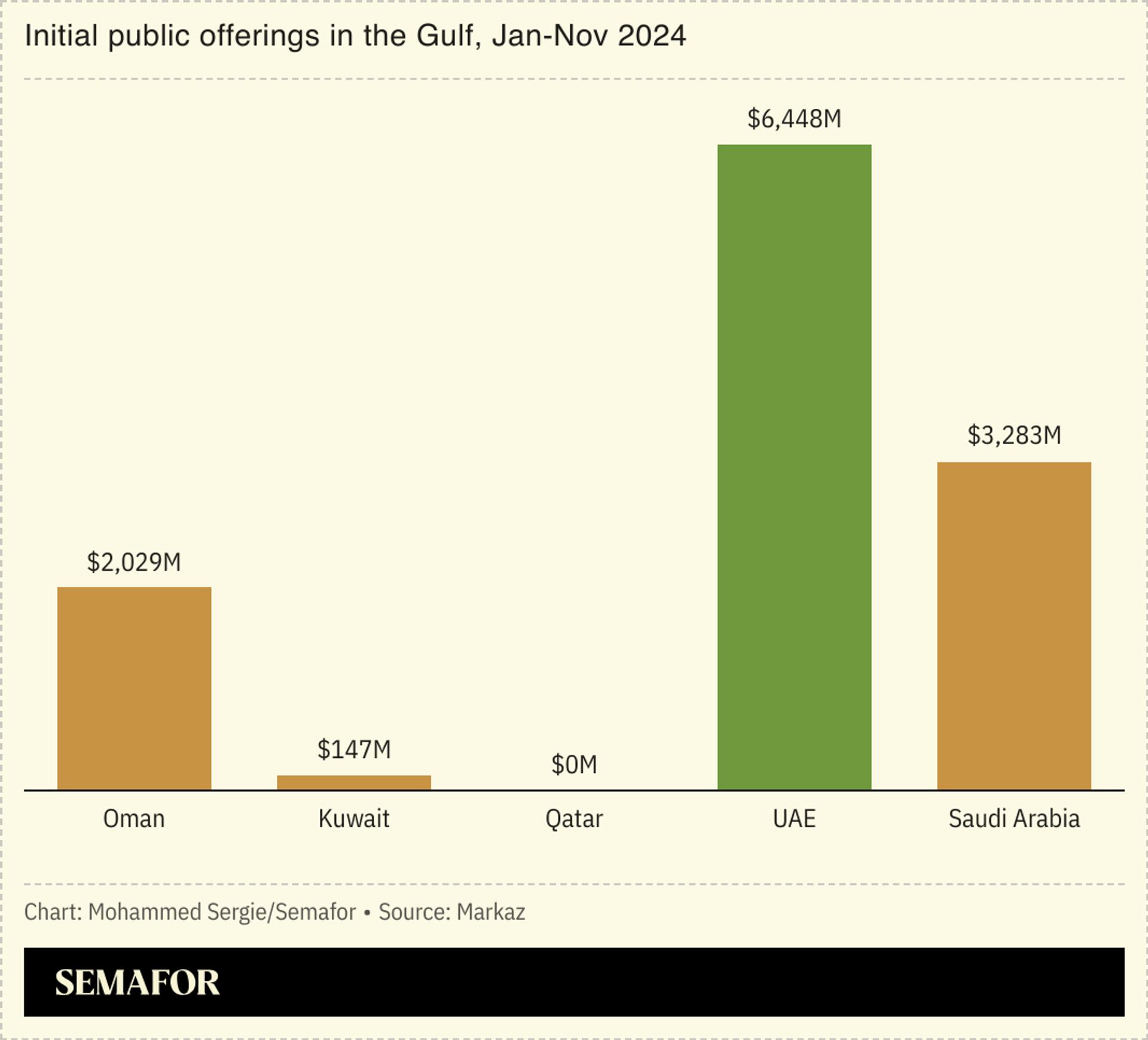

The capital markets in the Middle East are currently learning a brutal lesson in geography. For the better part of three years, the Riyadh and Dubai exchanges operated in a vacuum of prosperity, seemingly detached from the tectonic shifts of global inflation and high interest rates. That insulation has evaporated. As the shadow war between Iran and Israel spills into direct, kinetic confrontation, the world’s most active pipeline for initial public offerings is choking on the smoke. Investors who once viewed the region as a safe harbor for high-yield dividends are now recalculating the cost of proximity to a potential regional conflagration.

The math of the Gulf IPO boom was simple. State-owned giants, particularly in energy, logistics, and healthcare, were being carved up and sold to the public to fund ambitious national transformation projects like Saudi Arabia’s Vision 2030. It worked. In 2023, while the rest of the global listing market was in a deep freeze, the Middle East accounted for a staggering percentage of total deal volume. But the recent escalations involving Iran have introduced a "war premium" that no balance sheet can easily offset.

The End of the Gulf Exception

For a long time, regional bourses behaved as if they were located in Switzerland rather than the heart of the Levant. Local retail investors, flush with cash and encouraged by government mandates, crowded into every new offering. Institutional players from New York and London followed, lured by the promise of 7% dividend yields and a currency pegged to the dollar.

That confidence has been shaken. The core issue isn't just the fear of physical damage to infrastructure, though that remains a peripheral concern for oil installations. The real threat is the sudden evaporation of liquidity. When the threat of a wider war looms, "hot money" is the first to leave. International fund managers are not just looking at the profitability of a Saudi tech firm or an Emirati utility; they are looking at the Strait of Hormuz.

The Strait serves as the primary artery for the very commodities that fuel these economies. Any prolonged disruption there doesn't just raise oil prices; it paralyzes the logistical certainty required for the companies currently seeking to go public. If a logistics firm cannot guarantee its shipping lanes, its valuation during an IPO roadshow becomes a work of fiction.

Valuation Gaps and the Retail Retreat

The disconnect between what sellers want and what the market will bear is widening. Government-linked entities in the region are used to fetching premium valuations based on their monopoly status and sovereign backing. However, global investors are now demanding a significant discount to compensate for the geopolitical instability.

This tension creates a "valuation gap" that can kill a deal before it even reaches the subscription phase. We are seeing a quiet wave of postponements. While official statements usually cite "market conditions" or "internal restructuring," the reality is that the books aren't filling up at the desired price points.

- Institutional Caution: Global pension funds are tightening their risk parameters. A portfolio manager in Chicago faces a difficult conversation with their board if they increase exposure to Riyadh while missiles are in the air.

- Retail Exhaustion: Local investors, who provided the "floor" for many previous IPOs, are becoming wary. They see their existing holdings dipping and are less inclined to dump more savings into new, uncertain listings.

- The Cost of Hedging: For those who do stay, the cost of insuring these investments via Credit Default Swaps (CDS) has climbed, eating into the very dividends that made these stocks attractive in the first place.

The Saudi Engine Under Pressure

Saudi Arabia is the undisputed heavyweight of this market. The Tadawul exchange has been the stage for some of the largest listings in history. The Kingdom needs these IPOs to succeed. They are not merely financial transactions; they are the primary mechanism for transferring wealth from the state to the private sector and generating the capital needed to build cities like Neom.

The tension with Iran puts the Kingdom in a precarious position. To keep the IPO pipeline moving, Saudi authorities need a stable environment. Yet, the regional dynamics are pulling in the opposite direction. If the Kingdom has to divert more of its budget toward defense and regional security, the "investment story" of its non-oil economy becomes harder to sell.

Consider a hypothetical example of a mid-sized Saudi manufacturing company looking to go public. On paper, it has 20% year-on-year growth and a dominant market share. In a vacuum, it’s a "must-buy." But in the current climate, an analyst has to ask: What happens if supply chains through the Red Sea are permanently disrupted? What happens if regional tensions lead to a localized labor shortage? These questions are now front and center, whereas eighteen months ago, they were footnotes in the "Risk Factors" section of a prospectus.

The UAE Diversification Gambit

While Saudi Arabia deals with the heavy lifting of industrial transformation, Dubai and Abu Dhabi have focused on "lifestyle" and "tech" IPOs. From taxi services to supermarket chains, the UAE has been aggressive in privatizing its municipal assets.

The Emirati markets are perhaps even more sensitive to the Iran situation because of their role as a global hub. The UAE thrives on being the "everywhere" city—a place where people from all over the world live, work, and invest. That model relies heavily on the perception of total safety. When that perception is challenged, the "hub" status is at risk.

We are seeing a shift in the type of companies that are succeeding. Only the most "defensive" plays—those that provide essential services like water or electricity—are finding traction. The more speculative, growth-oriented companies are finding the doors closed. The appetite for a "disruptive tech startup" in a neighborhood facing potential conflict is understandably low.

The Fragility of the Dividend Model

The primary hook for Middle Eastern IPOs has always been the dividend. Unlike Silicon Valley IPOs, which promise future growth, Gulf IPOs promise immediate cash. This has been a winning strategy in a high-interest-rate environment because the yields often outpaced what investors could get from bonds.

However, the war premium is beginning to outrun the dividend yield. If an investor expects a 5% currency devaluation or a 10% market correction due to a sudden escalation, an 8% dividend yield is no longer a net gain. The fundamental math that sustained the 2022-2023 boom is breaking down under the weight of ballistic reality.

Defensive Posturing by Sovereign Wealth Funds

In response to the cooling interest from abroad, we are seeing a "circling of the wagons." Sovereign wealth funds (SWFs), such as the Public Investment Fund (PIF) in Saudi Arabia and Mubadala in Abu Dhabi, are being forced to step in as "anchor investors" more frequently.

While this ensures that the IPO actually happens, it defeats one of the primary purposes of the listing: attracting foreign direct investment (FDI). If the state is simply selling a company to its own sovereign fund or to local banks it largely controls, it’s just moving money from one pocket to another. It doesn't bring in the fresh, external capital required for long-term economic expansion.

The Role of Global Energy Prices

The irony of the Iran conflict is that while it threatens the IPO market, it often drives up the price of oil. Normally, higher oil prices are good for Gulf economies. They swell the coffers of the state and provide more capital for investment.

But this time is different. The correlation between high oil prices and high stock prices in the region has decoupled. Investors now see high oil prices as a "danger signal" of impending supply shocks rather than a sign of healthy demand. The "petrodollar recycling" that used to fuel local stock markets is being offset by the sheer uncertainty of what comes next. A company that exports petrochemicals might see higher margins when oil prices rise, but if it can't ship those chemicals because of a maritime blockade, the paper profits are meaningless.

The Liquidity Trap

The most significant danger to the region’s capital markets is the "liquidity trap." This occurs when investors become so fearful of a sudden downturn that they stop trading altogether. We are seeing the early signs of this in the secondary markets. Volumes are thinning. When volumes thin, volatility increases.

For a company looking to go public, a volatile secondary market is a nightmare. It makes "pricing the deal" almost impossible. If a similar, already-public company is swinging 5% in value every day based on the latest headlines from Tehran or Tel Aviv, how do you convince a new investor that your IPO price is "fair"?

The Shift to Private Equity

Because the public markets are becoming so erratic, some of the region's most promising companies are looking toward private equity instead. This is a quiet but significant shift. By staying private, these companies avoid the daily scrutiny of a geopolitical news cycle.

However, this is a setback for the "democratization of wealth" that many Gulf leaders promised. If only elite private equity firms can participate in the growth of the region's best companies, the broader public misses out. It also slows down the development of the robust, transparent financial ecosystems that these countries need to become global financial centers.

The Geopolitical Discount is the New Normal

It is a mistake to think that the IPO market will simply "snap back" to its previous highs once the current tension cools. The events of the past few months have recalibrated the risk models of every major investment bank. The "Geopolitical Discount" is now a permanent fixture of the Middle Eastern balance sheet.

Investors have been reminded that the region's prosperity is inextricably linked to its security. You cannot have a world-class financial market in a theater of war. The era of "easy IPOs" fueled by blind optimism and high dividends is over. What remains is a market that must work twice as hard to prove its stability.

The companies that do successfully list in this environment will have to be more than just profitable; they will have to be "war-proof." They will need to demonstrate diversified supply chains, domestic-focused revenue streams, and cash reserves that can withstand prolonged periods of regional instability.

The pipeline isn't dead, but the water flowing through it is getting much colder. Dealmakers are now looking at 2027 and 2028 for their "big exits," hoping that the current fever breaks. But in a region where history often repeats itself with violent regularity, hope is not a financial strategy. The Gulf is discovering that while you can build a city in the desert, you cannot build a market that ignores the horizon.

Stop looking for the "recovery" and start looking for the "realignment." The winners won't be the ones waiting for peace; they will be the ones who figure out how to operate in a state of permanent, managed friction. This is the new baseline for doing business in the world's most volatile backyard.

The era of the Gulf exception has officially ended.

Next, you might want to look into how local currency pegs are holding up under this increased pressure, as that’s the final domino in the regional stability narrative.