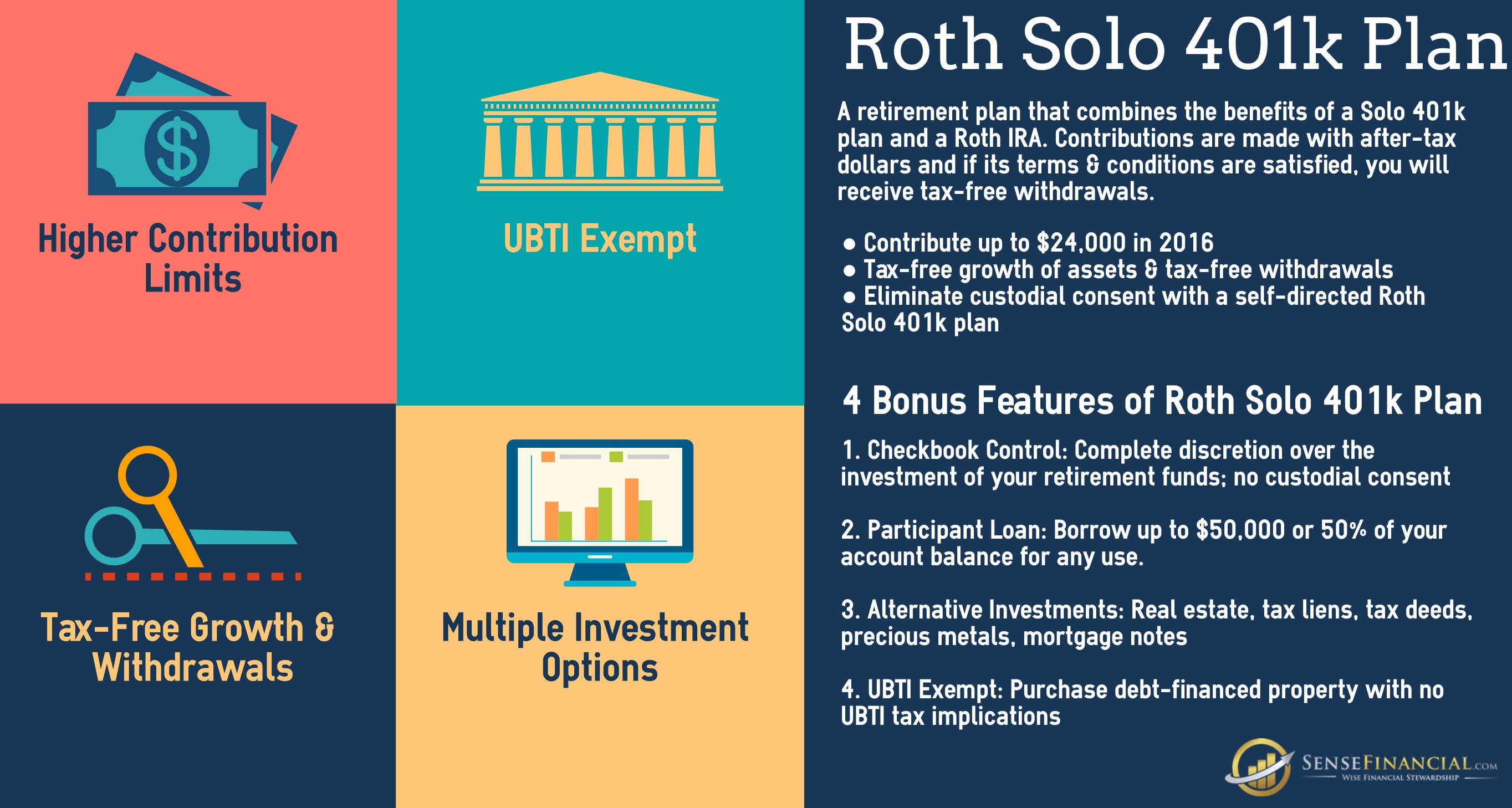

The era of the "stealth" tax break for America’s highest earners is ending. On January 1, 2026, a massive structural shift in how 401(k) plans operate will go into effect, stripping away the ability for those earning over $150,000 to lower their current tax bill through catch-up contributions. If you are 50 or older and your W-2 wages in 2025 crossed that threshold, the IRS no longer wants your "pre-tax" promises. They want their cut now.

Under the SECURE 2.0 Act, any catch-up contributions made by these high earners must be funneled into Roth accounts. This means you pay income tax on that money today in exchange for tax-free withdrawals decades from now. For a professional in the 32% or 35% tax bracket, this isn't just a technicality. It is a mandatory loss of a deduction that has, for years, been a cornerstone of late-career wealth preservation. Building on this topic, you can find more in: The Childcare Safety Myth and the Bureaucratic Death Spiral.

The Revenue Grab Hiding in Plain Sight

Washington rarely gives without taking. While SECURE 2.0 was marketed as a way to "expand" retirement access, the mandatory Roth transition for catch-up contributions serves a very specific purpose: budget balancing. By forcing high-income savers to pay taxes on their contributions immediately rather than deferring them until retirement, the government pulls forward billions in tax revenue to help offset the cost of other provisions in the bill.

The mechanism is simple but rigid. If your prior-year FICA wages (specifically the amount in Box 3 of your W-2) exceeded $150,000, you lose the choice. You can still contribute the extra $8,000 allowed for those 50 and older—or the enhanced $11,250 "super catch-up" for those aged 60 to 63—but you must do it with after-tax dollars. Observers at CNBC have provided expertise on this matter.

The $150,000 Line in the Sand

| Participant Detail | 2026 Rule Change |

|---|---|

| Prior Year Wages (2025) | Must be below $150,000 for pre-tax catch-up. |

| Standard Catch-up (50+) | $8,000 (Must be Roth for high earners). |

| Super Catch-up (60-63) | $11,250 (Must be Roth for high earners). |

| Base Deferral Limit | $24,500 (Can still be pre-tax for everyone). |

The Plan Sponsor Dilemma

This isn't just an individual headache; it is a corporate liability. Many older 401(k) plans do not currently offer a Roth component. Here is the "poison pill" in the legislation: if a company’s plan does not have a Roth option, no one in that company who earns over the threshold can make catch-up contributions at all.

Corporate benefits departments are currently scrambling. To keep their senior leadership and highest-paid talent happy, they must amend their plan documents and update payroll systems to accommodate Roth accounting. If they fail to do so by the 2026 deadline, their most experienced employees will be legally barred from "catching up," effectively capping their retirement savings at the base $24,500 limit.

This creates a hidden pressure on small-to-medium businesses. The administrative cost of adding Roth features isn't zero. Yet, the cost of losing a competitive benefits package—and the resulting talent drain—is far higher.

Why the Math Might Not Work for You

Financial advisors often champion the Roth 401(k) as the holy grail of retirement. They point to the "tax-free growth" and the lack of Required Minimum Distributions (RMDs) as undeniable wins. But for a 55-year-old executive at the peak of their earning power, the math is more cynical.

Imagine a taxpayer in a high-tax state like California or New York, sitting in a combined federal and state bracket of 45%. By losing the pre-tax deduction on an $8,000 catch-up, they are effectively losing **$3,600** in immediate cash flow. To "break even" on that Roth contribution, they have to bet that their tax rate in retirement will be equal to or higher than 45%.

For many, that is a losing bet. Most retirees see their income drop, placing them in significantly lower brackets. By forcing the Roth treatment now, the IRS is essentially locking in a high-tax payment on money that could have been taxed at a much lower rate fifteen years later.

Navigating the "Super Catch-Up" Complexity

One of the few "gifts" in the 2026 landscape is the Super Catch-Up. For a narrow window—specifically ages 60, 61, 62, and 63—the limit jumps to $11,250.

But don't expect a smooth ride. This provision creates a "sandwich" effect.

- At age 59, you get the standard $8,000 catch-up.

- At age 60, it spikes to $11,250.

- At age 64, it drops back down to $8,000.

This volatility requires precision in payroll elections. If you turn 64 mid-year, you must ensure your contributions don't accidentally exceed the reverting limit, which could trigger IRS penalties and the need for "corrective distributions"—a bureaucratic nightmare that involves your employer’s HR department and the return of over-contributed funds.

The One Remaining Pre-Tax Lifeboat

If you are a high earner and the loss of that deduction stings, there is one often-overlooked alternative: the Health Savings Account (HSA).

While 401(k) catch-ups are going Roth, HSA contributions remain "triple tax-advantaged." They are pre-tax going in, they grow tax-free, and they are tax-free coming out for medical expenses. More importantly, after age 65, an HSA essentially functions like a traditional IRA; you can withdraw money for any reason and only pay ordinary income tax, with no 20% penalty.

For 2026, the family contribution limit for an HSA is $8,750, plus a $1,000 catch-up if you are 55 or older. If you've been forced into a Roth 401(k) catch-up, maximizing your HSA is the only way to claw back some of that lost tax-deductible territory.

A New Strategy for the Final Stretch

The 2026 changes signal a fundamental shift in how the government views "high earners." You are no longer being encouraged to defer taxes; you are being required to prepay them. This isn't a suggestion—it’s a mandate that will be enforced through your employer's payroll software.

The strategy for the next decade is no longer about just "maxing out." It is about tax diversification. You will likely end up with a "hybrid" 401(k)—a large bucket of pre-tax money from your earlier career and your base contributions, and a smaller, mandatory Roth bucket from your 50+ catch-up years.

Managing these two distinct tax treatments will be the defining challenge for retirees in the 2030s and 2040s. You'll need to decide which bucket to drain first to stay under certain tax thresholds, especially when Medicare Part B premiums (IRMAA) start looking at your reported income.

Check your 2025 W-2 the moment it arrives. If Box 3 says $150,001, your 2026 retirement plan just got more expensive. Use the remaining months to talk to your payroll department and ensure they are actually ready for the Roth transition, because if they aren't, you're the one who loses the ability to save.

Ensure your employer has officially updated their plan document to include a Roth provision before the end of the year.